| |

|

|

... |

|

Term Life Insurance by Top

Rated Companies

More term companies

equals the best opportunity to obtain the lowest term quote!

Offering the Largest Selection of

Top-Rated Companies Instantly!

Why is this important?

Personalized

Tele-Application for All Companies, Right Over the

Phone!

For the serious shopper who would like a seasoned

professional to assist them-

"how term life insurance

works", "return of premium term life insurance",

"no exam term life insurance" and "what is term life

insurance" will be explained on this page.

|

Federal Estate Tax Planning

|

|

|

Note: In all cases, when implementing an estate plan, legal advice is a

must!

Federal Estate Tax Planning is a must or, the government may take a large part of

your estate. Figuring estate tax

is complex, and the phase out of the tax through decreases in the

top estate-tax rate

and increases in the estate-tax credit makes the computation even

more complicated. However, to effectively plan your estate, you need

at least a basic understanding of

how the tax works.

Every individual is allowed a credit that permits a certain

amount in assets to pass free of estate and gift tax. So, if

your total taxable estate and lifetime gifts are less than

or equal to the applicable credit exclusion amount (see

below), no federal estate tax will be due.

(The gift-tax exclusion amount is $1 million.) To

illustrate: In 2007, the credit will offset $780,800 in

estate taxes. If you die in 2007 with a

taxable estate

of $2.1 million, having made no taxable gifts during life,

the tentative estate tax will be $825,800. However, assuming

your estate has no adjustments other than the estate-tax

credit, the actual tax will be $45,000 ($825,800 –

$780,800).

ESTATE VALUE

For a general idea of how much tax, if any, will be due on

your estate, estimate the current value of your estate

worksheet. Then subtract allowable deductions. These

deductions may include, but aren’t limited to:

|

|

• |

Estate administration fees; |

|

|

|

• |

Funeral expenses; |

|

|

|

• |

Valid debts, such as your mortgage and unpaid property

or income taxes; |

|

|

|

• |

Transfers for public, charitable, and religious uses;

and |

|

|

|

• |

Bequests to your surviving spouse (see

Unlimited Marital Deduction,

discussed in next section).

|

|

Next, add in the value of any taxable lifetime gifts you have made.

Check this amount against our tax

table to get an idea of the amount of tax your estate would owe if

you should die in 2007–2008.

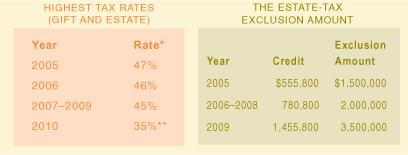

TAX RATES AND EXCLUSION AMOUNT

The generation-skipping transfer tax is assessed at a flat

rate equal to the top gift- and estate-tax rate.

**Gift tax only. Estate and generation-skipping transfer taxes

(discussed later) are repealed in 2010.

THE GENERATION-SKIPPING TRANSFER TAX

Another possible concern for the near future is the

generation-skipping transfer (GST) tax. This tax

could come into play if you want to leave your assets in a way that

will benefit your grandchildren or

other persons more than a generation younger than you. The GST tax

rate is steep — equal to the highest federal estate-tax rate (see

the

Tax Rates and Exclusion Amount

table). GST tax, which is

being phased out on the same schedule as the estate tax, must be

paid

in addition to

estate and

gift tax.

The purpose of

the GST tax is to prevent families from sidestepping a generation’s

worth of estate

taxes by transferring assets to grandchildren, rather than to

children. GST tax applies both to indirect transfers made in trust

(for example, a trust that benefits your child first and, then, your

grandchild after your child’s death) and to “direct skips,”

transfers made directly from you or from a trust you create to a

grandchild or another person two or more generations below your

generation.

A cumulative

$1.5 million GST tax exemption gives you leeway to transfer up to

that amount to your grandchildren or others free of the GST tax. If

you and your spouse agree to split gifts, together you can give your

grandchildren up to $3 million without incurring the GST tax. This

exemption tracks the

estate-tax exclusion amount (see the

Tax Rates and Exclusion Amount

Table).

The GST tax

does not apply to direct transfers and certain transfers from trusts

you make to a

grandchild whose parent — your child — is deceased. GST-tax-free

transfers to “collateral” heirs

(such as a grandniece or grandnephew) may also be possible under

limited circumstances.

Another possible concern for the near future is the

generation-skipping transfer (GST) tax. This tax

could come into play if you want to leave your assets in a way that

will benefit your grandchildren or

other persons more than a generation younger than you. The GST tax

rate is steep — equal to the highest federal estate-tax rate (see

the

Tax Rates and Exclusion Amount

table). GST tax, which is

being phased out on the same schedule as the estate tax, must be

paid

in addition to

estate and

gift tax.

The purpose of

the GST tax is to prevent families from sidestepping a generation’s

worth of estate

taxes by transferring assets to grandchildren, rather than to

children. GST tax applies both to indirect transfers made in trust

(for example, a trust that benefits your child first and, then, your

grandchild after your child’s death) and to “direct skips,”

transfers made directly from you or from a trust you create to a

grandchild or another person two or more generations below your

generation.

A cumulative

$1.5 million GST tax exemption gives you leeway to transfer up to

that amount to your grandchildren or others free of the GST tax. If

you and your spouse agree to split gifts, together you

can give your grandchildren up to $3 million without incurring the

GST tax. This exemption tracks the estate-tax exclusion amount (see

the Tax Rates and

Exclusion Amount

Table).

The GST tax

does not apply to direct transfers and certain transfers from trusts

you make to a

grandchild whose parent — your child — is deceased. GST-tax-free

transfers to “collateral” heirs

(such as a grandniece or grandnephew) may also be possible under

limited circumstances.

Currently, capital gains taxes are more of a financial planning

consideration than an estate-planning

one. But this is likely to change in the future. With the

estate-tax repeal comes a change in the way

capital gain on inherited property is taxed.

You pay

capital gains tax on gains realized when you sell property that

has increased in value while you’ve owned it. Your gain (or

loss) for capital gains tax purposes is usually determined by

using your “basis” in the property. Basis generally refers to

the amount you paid to acquire the property, plus or minus

various adjustments that may be required after acquisition (for

items such as depreciation, reinvested dividends, and the cost

of capital improvements). Your gain is the value of the property

in excess of your basis.

When you

give someone assets during your lifetime, your basis (or the

fair market value of the assets,

if less) on the gift date is carried over and becomes the

recipient’s basis. If the recipient later sells the

gift assets, he or she is liable for capital gains tax on the

assets’ appreciation both

before

and after

you made the gift.

Inherited

property is treated differently. It usually receives a “step-up”

in basis to its fair market value at the time of the owner’s

death. So, if you leave property to your son and he later sells

it, he’ll be responsible for capital gains tax only on the

appreciation generated after your death. However, as of 2010,

new rules apply for determining inherited property’s basis. The

new rules limit basis step-ups

and, in many cases, will result in significantly higher capital

gains taxes on the sale of inherited property.

In 2010,

each estate generally will be able to increase the basis of

property transferred only up to a

total of $1.3 million. The basis of property transferred to a

surviving spouse may be increased by an additional $3 million

for a total of $4.3 million. These amounts will be adjusted

annually for inflation.

Some

property — tax-deferred money in retirement plans and Individual

Retirement Accounts, for example — won’t be eligible for even

the limited step-up. Any property that isn’t allocated a basis

step-up will pass to your heirs and beneficiaries with a

“carryover” basis equal to the

lesser

of (1) your adjusted basis in the property or (2) the property’s

fair market value on the date of death.

COMPARING CAPITAL GAINS TREATMENT

Earl

owns closely held stock that he bought at $10 a share. When he

dies in 2010, his daughter Gretchen inherits the stock, now

valued at $500 a share. Shortly after his death, Gretchen sells

the stock for $500 a share. Under the new carryover basis rules,

Gretchen will have a capital gains tax bill of $98 on each share

sold (20% capital gains tax rate × $490 appreciation). If Earl

had died before 2010, Gretchen would have owed no capital gains

tax because her basis in the stock would have been stepped-up to

its value at Earl's death — $500 a share — and she wouldn't have

realized any capital gain on the sale.

NEXT

Author’s note:

The intent of this article by termlifeamerica.com is to

inform and motivate the general public into action.

One should consider only a qualified practicing legal individual or

entity, in the state in which you reside, to establish properly

drawn documents of this type.

SEE

Estate Planning Brochure

Related Topics:

|

|

|

|